Porfolio Finder¶

A Python library, based primarily around pandas, to identify an optimal portfolio allocation through back-testing.

API Documentation is available on Read the Docs.

Example Usage¶

Each of these examples make use of data.csv which provides returns for a handful of funds over 1970-2019.

Find best portfolio allocation to minimize the required timeframe to achieve a target value¶

from portfoliofinder import Allocations

Allocations(0.05, ['USA_TSM', 'WLDx_TSM', 'USA_INT', 'EM'])\

.filter('USA_TSM>=0.6 & WLDx_TSM<=0.2 & USA_INT>=0.3')\

.with_returns("data.csv")\

.with_regular_contributions(100000, 10000)\

.get_backtested_timeframes(target_value=1000000)\

.get_statistics(['min', 'max', 'mean', 'std'])\

.filter_by_min_of('max')\

.filter_by_max_of('min')\

.get_allocation_which_min_statistic('std')

Output

Statistic

min 14.000000

max 22.000000

mean 16.965517

std 2.809204

Name: Allocation(USA_TSM=0.65, WLDx_TSM=0.0, USA_INT=0.3, EM=0.05), dtype: float64

Find best portfolio allocation to maximize value with minimal risk over a fixed timeframe¶

from portfoliofinder import Allocations

Allocations(0.05, ['USA_TSM', 'WLDx_TSM', 'USA_INT', 'EM'])\

.filter('USA_TSM>=0.6 & WLDx_TSM<=0.2 & USA_INT>=0.3')\

.with_returns("data.csv")\

.with_regular_contributions(100000, 10000)\

.get_backtested_values(timeframe=10)\

.get_statistics(['mean', 'std'])\

.filter_by_gte_percentile_of(90, 'mean')\

.get_allocation_which_min_statistic('std')

Output

Statistic

mean 446560.590088

std 117448.007302

Name: Allocation(USA_TSM=0.6, WLDx_TSM=0.0, USA_INT=0.3, EM=0.1), dtype: float64

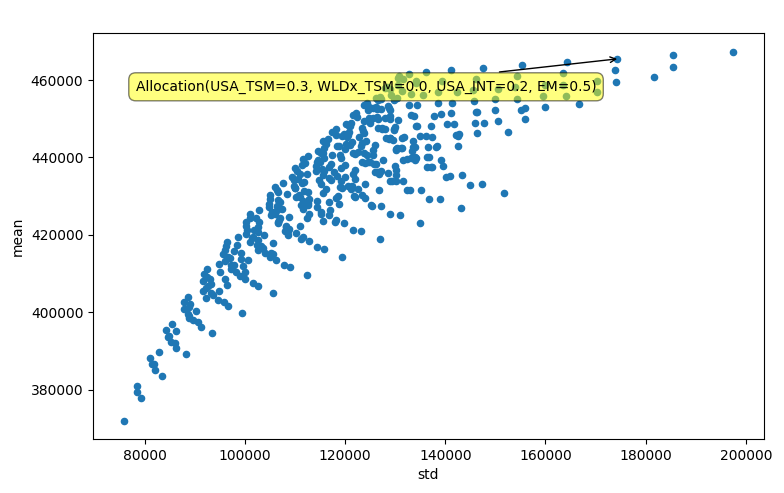

Graph statistics from multiple portfolio allocations to visualize their efficient frontier¶

from portfoliofinder import Allocations

Allocations(0.05, ['USA_TSM', 'WLDx_TSM', 'USA_INT', 'EM'])\

.filter('USA_TSM>=0.2 & USA_INT>=0.2')\

.with_returns("data.csv")\

.with_regular_contributions(100000, 10000)\

.get_backtested_values(timeframe=10)\

.get_statistics()\

.graph('std', 'mean')

Output